July 15, 2026

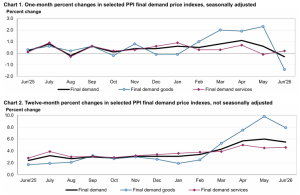

According to the U.S. Bureau of Labor Statistics, the Producer Price Index (PPI) for final demand fell 0.3% in June, seasonally adjusted. This follows a 0.6% advance in May and a 1.1% increase in April. On an unadjusted basis, the index for final demand increased 5.5% over the 12 months ended June.

The June decline was driven by final demand goods, which fell 1.4%, while final demand services prices rose 0.2%.

Excluding foods, energy, and trade services, the PPI for final demand increased 0.1%, following a 0.8% jump in May. Over the past year, this measure rose 5.1%.

Final demand goods

Prices for final demand goods declined 1.4%, the largest decrease since a 1.9% drop in July 2022. Leading the decline, energy prices fell 6.4%. Food prices moved down 0.6%, while goods excluding food and energy rose 0.2%.

A major contributor was a 12.0% drop in gasoline prices, which accounted for nearly two-thirds of the overall goods decline. Prices also fell for diesel fuel, jet fuel, fresh vegetables (except potatoes), crude petroleum, and thermoplastic resins and materials. Offsetting these declines, prices for plastic products advanced 1.6%, while residential electric power and potatoes also increased.

Final demand services

The index for final demand services rose 0.2%, following a 0.1% decline in May. Over 60% of the advance was attributable to trade services margins, which moved up 0.4%. Services excluding trade, transportation, and warehousing increased 0.1%, while transportation and warehousing services declined 0.1%.

A 13.0% jump in fuels and lubricants retailing margins accounted for half of the overall services gain. Additional contributors included increases in securities brokerage, dealing, and investment advice; furniture retailing; apparel, jewelry, footwear, and accessories retailing; loan services; and inpatient care. Declines were recorded in machinery and vehicle wholesaling margins, which fell 8.4%, as well as in food and alcohol wholesaling and deposit services.

Disclaimer:

Analyst Certification – The views expressed in this research report accurately reflect the personal views of Mayberry Investments Limited Research Department about those issuer (s) or securities as at the date of this report. Each research analyst (s) also certify that no part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendation(s) or view (s) expressed by that research analyst in this research report.

Company Disclosure – The information contained herein has been obtained from sources believed to be reliable, however its accuracy and completeness cannot be guaranteed. You are hereby notified that any disclosure, copying, distribution or taking any action in reliance on the contents of this information is strictly prohibited and may be unlawful. Mayberry may effect transactions or have positions in securities mentioned herein. In addition, employees of Mayberry may have positions and effect transactions in the securities mentioned herein.